Complete Guide to Pricing Strategies for Increasing Profit Margins

Introduction to Pricing Strategies

Even for businesses with an established customer base, remaining competitive with product pricing within their market is essential for customer loyalty and reach. In order to make a strategy work, companies must find an effective pricing strategy and quality of goods ratio that promotes customer satisfaction and their bottom line.

Pricing strategies are various ways businesses can price their goods and services. A company can price their items by taking the following into account-

- Market conditions

- Competitor prices

- Account segments

- Trade margins

- Variable costs

- Operation costs

- Consumer demand

- Input cost

While many companies are quick to set high prices in hopes of better profit margins, increasing cost could send customers to competitors. On the other hand, low pricing could break the bottom line. Therefore, it is vital to find a pricing strategy that provides a healthy balance for the company and consumers.

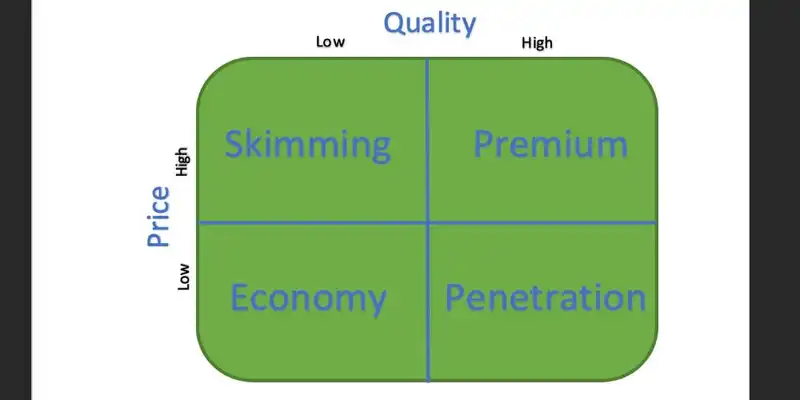

The Pricing Strategy Matrix

There is a pricing method for every type of business, from small start-ups to large enterprises.

For example, when Netflix was debuting its streaming service, it was using a model known as market penetration pricing, or a gradual sale price increase. They entered the market with a low price of $7.99 a month. However, as Netflix gained popularity, they raised the amount and implemented competitive pricing strategies. Netflix now offers different streaming plans that range from $8.99 - $15.99 a month.

However, what worked for Netflix may not necessarily work for every other business. This is when the pricing matrix comes in.

The pricing matrix is a useful tool to determine what pricing model works best for a company. The matrix is set up in 4 quadrants, with product quality on the x-axis and product price on the y-axis. This graph helps businesses determine prices by considering an item's quality and cost.

Economic Pricing

Economy pricing falls in the bottom, left quadrant of the matrix on the low end of quality and price. Businesses that use this pricing model must also have lower overhead costs than competitors to turn a profit.

While using cheaper materials to produce low-quality goods does reduce production costs, quality within the matrix does not directly refer to product grade. Instead, quality in this case relates to any good or service that doesn't enhance the customer's experience. Low-quality experiences may include a limited range of goods or less than an ideal selling environment.

Advantages

- Setting lower prices helps companies survive during economic downfalls when consumers seek the lowest-priced items.

- Lowballing the market price gives companies an edge among the industry's competition.

- Small businesses may find it difficult to implement economic pricing, as they would not receive the high-volume discounting for product orders that are needed to execute this strategy successfully.

- The economic pricing model is a popular strategy, meaning the competition is high. Consumers are always looking for the lowest price and are willing to change retailers to find it. Therefore, businesses must be willing to alter their prices more than once to continually regain customers and remain a competitor. This often leads to varying profit margins and unstable demand forecasting.

Penetration Pricing

The penetration pricing model lands in the bottom, right quadrant, catering to high quality and low price. This model is often used by businesses anticipating an influx of customers ready to buy their affordable service or good. Once a stable consumer base is formed, the company can increase its prices and switch to a strategy that caters to higher premiums.

Advantages

- Penetration pricing is the most effective strategy to introduce a high-quality product in a competitive market.

- The cost elasticity provided in this method allows businesses to increase the product price as needed.

- The initial low pricing can limit profit margins until prices rise.

- Setting the starting cost too low can make the product look cheap, making it hard to attract customers.

- Raising prices may come with customer resistance.

Price Skimming

In the top, left quadrant, price skimming targets low-quality products with high prices. By selling an inexpensive product at a high price, businesses can generate much revenue in a short period.

However, the high-profit margin has a short window before costs must drop to meet the market price. The skimming strategy is often used in novelty markets, such as bookstores, that frequently launch new products.

Advantages

- The high prices maximize profits.

- Production costs are guaranteed to be covered by skimming from revenue during the high-profit window.

- Customer loyalty can be hard to attain as consumers may become upset when prices suddenly fall after they had paid the premium product price.

- Timing is everything in this method. If the window of high prices is open too long, customers could lose interest. However, if the window is too short, the business will not gain enough profit.

Premium Pricing

The premium pricing model is in the top right quadrant that caters to high quality and price. This method is exclusive and contains brands with an expensive image that can afford to set high costs due to their quality and demand.

Advantages

- Premium prices mean high-profit margins.

- An expensive price tag promotes your brand's essence.

- A company must build up to this strategy, as launching an expensive product doesn't gain market shares initially.

- Riding the fine line between over and under-producing is crucial. Lack of product means a significant loss of profits while overproducing wastes capital in production and materials.

Types of Pricing Strategies

While the matrix provides broad methods on how to approach pricing goods and services, there are several pricing value strategies that can be applied on a more specific basis.

1. Competition-Based

This pricing strategy negates the production cost of the item and consumer demand and instead focuses on the existing market price for the goods or services. By using the competitors' charges as a reference, businesses can slightly lower costs below the going rate to attract more demand. Businesses can also choose to set a higher price than other companies to promote their brand identity while remaining competitive.

2. Cost-Plus

The cost-plus method focuses only on how much it costs a company to produce a good. This strategy is also known as markup pricing because businesses can mark up their prices based on how much profit they'd like to earn.

To implement cost-plus pricing, a business must first determine how much it costs to make their product then determine their desired profit. This model is commonly used by retailers who mark up their items from the initial production cost. For example, if a shirt costs $10 to make and the company would like a $7 profit from each unit, they would markup each shirt to $17.

3. Dynamic

Also known as surge, demand, and time-based pricing, the dynamic strategy offers cost flexibility to reflect the overall demand. Management applies algorithms and forecasting systems to predict demand and adjust costs accordingly. Businesses that use dynamic pricing include airlines, venues, and utility companies where the demand for services fluctuates.

4. Freemium

This method combines free and premium to offer a basic product at a low price in hopes that customers will eventually pay extra for an upgrade. Software companies and application developers often use this approach when pricing their services. Usually, the free services are offered as a "lite" version with limited features. Then several plans are laid out that slowly increase in cost and features.

5. High-Low

High-low, or discount pricing, initially prices an item high but eventually lowers the cost concerning its relevance. Many businesses practice this through discounts, clearance sections, and end of the year sales to clear out shelves for new products while regaining some capital.

6. Value-Based

Value-based pricing is when a company uses what the majority of the consumers are willing to pay as their base cost. While companies can choose to increase the price for larger profit margins, reflecting consumer price recommendations have been found to increase satisfaction and loyalty.

This method requires consumer insight and willingness to fluctuate prices according to the demand. Businesses can utilize sales data from POS systems and forecasting software to observe past consumer spending habits and identify purchasing trends, then update pricing strategies accordingly. This sort of flexibility can create sporadic changes in cost and sales.

7. Bundle

To use the bundle pricing strategy, a company needs to group several products or services together at one price point. These bundles can include exclusive goods to attract more customers or promote a single product with complimentary extras. Offering bundles can introduce more products to customers and make them feel as if they got a bargain, increasing customer satisfaction.

8. Psychological

The psychological pricing strategy has many elements that businesses can utilize. The most common type of psychological pricing is the 9-digit effect," where an item is priced just a cent lower than the rounded number. For example, a customer is more likely to buy an item that costs $9.99 than if it was priced at $10 because they feel that they are getting a better deal.

Other types of psychological pricing involve formatting, font, size, and color of price tags shown to boost sales in different industries. For example, placing an item on sale next to a similar, more expensive product has shown to promote sales for the marked down merchandise.

9. Geographic

This method considers the distributor's geographic location when pricing a product. Demand and market prices vary significantly around the world due to cultural differences, varying economic conditions, and trends. Therefore companies prevalent in different nations must reflect these factors in their prices.

Considering Demand When Developing Pricing Strategies

Price elasticity of demand is a calculation to see how price flexibility affects an item's demand. A product is inelastic if an increase in its price does not affect customer demand levels. This is apparent in the fuel industry. On the other hand, when a product suffers in sales because of a rise in cost, it is considered to be elastic, shown in the entertainment industry.

Businesses can calculate an item's price elasticity using the equation-

Price elasticity of demand = % change in quantity / % change in price

Ideally, businesses want their products to be inelastic, so their demand, sales, and profit remain consistent.

Considering the Industry When Establishing Pricing Strategies

Businesses should consider their industry and respective markets when choosing a pricing strategy. Some methods are catered more towards services, while others are only effective when dealing with physical goods. Common industries and their respective pricing models include-

Physical Product-Based Businesses

Physical items require additional investment such as shipping, production, and carrying costs that should be considered when setting prices. Recommended pricing strategies for product-based businesses include-

- Cost-plus

- Competition-based

- Premium

- Value-based

While digital products do not require production costs, businesses should product price based on brand and industry reflection. Recommended pricing strategies are-

- Competition-based

- Freemium

- Value-based

Pricing menu items involves physical inventory costs, plus overhead, and service costs that must be considered. However, demand, market trends, location, and brand should also influence pricing decisions. Recommended strategies for restaurants include-

- Cost-plus

- Premium

- Value-based

Investments in holding events centers around a marketing strategy and organizing costs, as well as the entertainment. Since the demand for events can fluctuate, the recommended pricing strategies include-

- Competition-based

- Dynamic

- Value-based

The value of work is the primary focus when pricing services, as there is no tangible product to access. Recommended pricing strategies are-

- Hourly

- Project-based

- Value-based

Nonprofit organizations need to set prices to elongate operations while considering the costs of campaigns and communication. Recommended pricing strategies include-

- Competition-based

- Dynamic

- Hourly

Evaluating homes includes accessing competition, location, cost of living, and demand. Recommended pricing strategies include-

- Competition-based

- Dynamic

- Premium

- Value-based

There are numerous elements to consider when pricing a company within the complex industry of manufacturing. Among the most critical factors are the demand, production costs, average material usage, daily marketing sales, and inventory costs. Therefore, the recommended pricing methods include-

- Competition-based

- Cost-plus

- Value-based

When selling products online, businesses must price items according to demand as well as the ideal profit margin to compensate for marketing strategy ventures. Therefore, the recommended pricing methods include-

- Competition-based

- Cost-based

- Dynamic

- Freemium

- Value-based

- Penetration

How Automated Ordering Increases Profit Margins

A case study shows that nearly 30% of businesses are not maximizing profit margins due to inadequate pricing. A profit margin refers to the ratio or percentage of a dollar that each sale contributes to the gross profit.

Companies also tend to limit their profit margins by inefficient stock control. As production and inventory costs increase, profit margins decrease. Businesses can boost profit margins by optimizing their stock levels so capital is not wasted on unnecessary expenditures.

Stock replenishment systems automatically regulate inventory spending and notify users of any price changes from vendors. Management can search in the system by local vendors or items to find the best value product pricing, guaranteeing ideal price points, and quality.

An optimized ordering system allows companies to offer affordable prices to consumers, boosting customer loyalty, satisfaction, and profit margins. Replenishment software also alerts management of spending ratios, inventory spending, and in-real-time stock levels. Access to this information gives businesses the opportunity to discover where capital can be gained from limiting inventory expenditures.

Pricing items is a sensitive matter for both the business and customers. Incorrectly setting a cost can significantly reduce the gross profit or send customers straight to competitors. By defining what factors are most important to a business's industry and choosing the appropriate pricing strategy, a company can increase its profit margins without sacrificing quality.

Must-Read Content

5 Top Tips for Profitable Product Bundle Pricing